Market Research Podcast

Jonathan Gelfand and Kerri Moriarty connect to discuss ways to structure market research to maximize customer feedback in the process of restructuring or developing a new cobrand program.

Jonathan Gelfand and Kerri Moriarty connect to discuss ways to structure market research to maximize customer feedback in the process of restructuring or developing a new cobrand program.

Earlier this month, Jonathan Gelfand offered his perspective on trends in the payment industry to Creditcards.com in an article featured on Yahoo! Finance. See what Jonathan has to say about the growing emphasis on cobrand credit cards and expanded card offerings in the full article available here.

Our own Jonathan Gelfand's work on understanding customer behavior can be seen on the featured columnist section of Loyalty360.org. Jonathan helps break down three key objectives for customer feedback:

The entire article can be seen on the site here. If you're not a member of Loyalty360, you can visit the article over here on our blog.

By: Jonathan Gelfand

The Credit Card Accountability Responsibility and Disclosure Act of 2009 shook the credit card market to its core. It was the first major legislation that profoundly impacted credit card regulation in recent memory. There were significant doom and gloom predictions at the time as to the impact of the act on customers, banks, and also partners in the co-brand market. To compound the complexity, the Durbin Amendment impacted economic decisions at banks as debit cards became less profitable, reducing the relative negative expected impacts on credit card portfolios. In October, the Consumer Financial Protection Board issued a report summarizing the results to date of CARD Act. The impacts of the CARD Act are modest.

Impacts for Co-brand Credit Card Programs

When CARD Act was approved, most programs weren’t directly impacted from a contractual perspective, although a few were when their banks renegotiated their contract. The overall economic environment impacted many more programs, but that can’t be directly attributed to CARD Act.

Indirectly almost all programs were impacted from a marketing budget perspective and an increased conservatism with respect to account approval and portfolio management. Attribution of the exact changes to CARD Act is difficult because they overlapped with the economic downturn. Although the cost of credit (fees and interest) were largely unchanged from before CARD Act, the availability of credit has declined substantially impacting the size of the market and hence the potential size for co-brand programs.

Cost of Credit

Leading up to CARD Act’s implementation in Q2 of 2010, the average retail annual percentage rate charged customers increased as banks pro-actively raised the cost of credit to customers. With the exception of deep sub-prime customers, all other cohorts are subject to higher finance charge interest rates than they were before the CARD Act. From this perspective, consumers didn’t do well with CARD Act’s intervention into the market.

For revolving accounts, the story is a little better with the average retail annual percentage rate remaining relatively constant, except for deep subprime customers the impact is largely moot or slightly negative. It is interesting to note that there has been a slight downward trend in interest rates that probably reflects profit optimization within revolving customer segments.

When fees are combined with the effective interest rate the picture shows that the total cost of credit for revolving customers is largely unchanged compared to the period before CARD Act. Net, CARD Act doesn’t appear to have negatively impacted the cost of credit for customers or revenue for banks except in the subprime market.

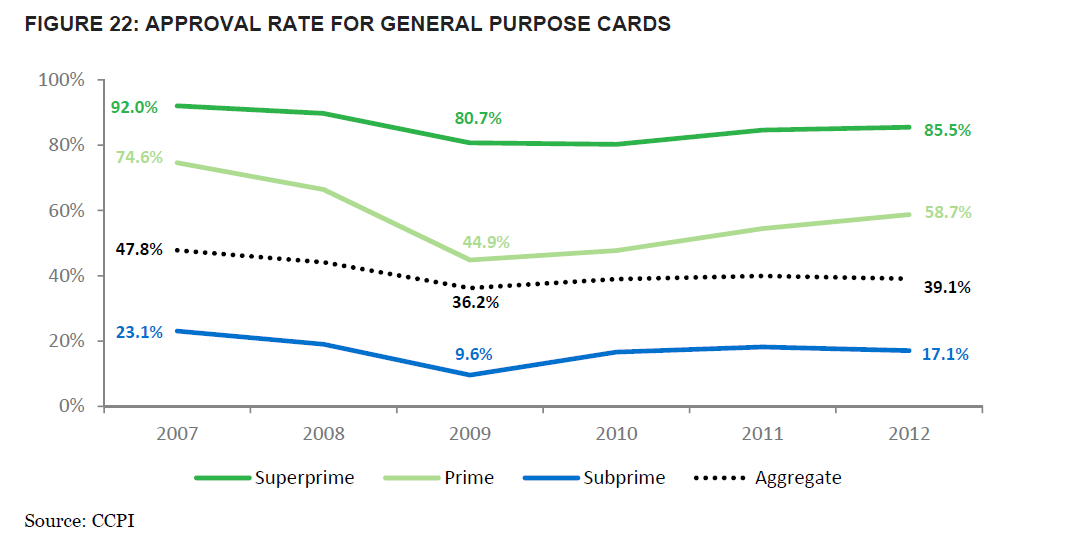

Credit Availability

Due to a combination of the recession and CARD Act, there was a sharp decline in new credit card accounts opened after 2007. Over the same period Private Label credit cards were much more consistent.

Part of the decline in new accounts is driven by a decrease in direct mail, the traditional work horse of credit card acquisition, but also by a decrease in approval rates across all levels of credit quality. This decrease is a concern to co-brand programs since a declined customer will have some negative impression of the sponsoring organization.

In addition, once an account is approved, there is a lower line issued. This is likely attributable mostly to the general economy. Since accounts tend to go bad at the limit while good accounts tend to not use the full limit, high lines reflect significant exposure.

Future Focus

The CFPB has informed the public that they will be looking at deferred credit disclosures and rules as well as rewards disclosures in the future. Both of these are important issues for co-brand program partners and should be tracked carefully to make sure that the programs maximize current contributions but are also well positioned for the future.

By: Jim Tierney

Launching a co-branded credit card program may not be a big deal in the U.S., but in Canada it’s a bit different especially when a non-bank – Toronto-based telecommunications company Rogers Communications – is involved, according to Sean Collins, Managing Member of Wellesley, MA-based Partner Advisors.

Rogers Communications recently cleared the final regulatory hurdle on its path to entering the financial services business and plans to start offering credit card services in conjunction with its new loyalty program – Rogers First Rewards -- next year.

Rogers Communications had been seeking a bank license since September 2011 and the Office of the Superintendent of Financial Institutions has granted authorization to “commence and carry on business.” Rogers officials have said a subsidiary will begin offering credit card services with a pilot program for select customers first, and general commercial availability will occur sometime in 2014.

Collins told Loyalty 360 that Canada has had co-branding for some time.

“I think the nuance here is that a non-bank has applied for and will receive permission to actually issue,” he said. “That is something the states have really backed off of.”

Collins cited Walmart’s failed bid to enter the financial services market.

“Basically, Walmart wanted to do banking and had secured a type of banking charter that looked as though they might actually do banking as a Walmart entity,” Collins explained. “There was a hue and cry around that from the banking community as you might imagine, and there was a great deal of pressure applied in Washington to prevent that from happening. There is some concern among regulators that non-bank banks might skew the system, and of course the branch bank down the street is loathe to compete with the likes of Walmart for bread and butter banking.”

What’s interesting, Collins added, is that with the financial crash and subsequent bank regulations applied in the U.S., “bread and butter banking (like checking accounts and debit cards) became a whole lot less attractive and banks could lose money on certain retail accounts – meaning that Walmart may have dodged a bullet.”

Collins discussed co-branded credit card programs in Canada compared to the U.S.

“Canada has a much smaller population than the U.S., and a different payments mix which leads to fewer programs,” he said. “Canadian consumers tend to carry fewer credit cards than their American counterparts. It isn’t so much of a case of longer, but a different marketplace requiring a holistically different strategy. Generally, the (Canadian) market is less hypercompetitive than the U.S. due to both the consumer differences as well as a different approach to regulations for banks and the payment networks (i.e. VISA, MasterCard, etc.).

Canadian consumers tend to be very interested in large “hub” rewards programs, like Air Miles, that attract a large base of consumers, Collins said.

“They are multi-merchant programs that also tie in manufacturers,” he said. “Those programs have been very successful in Canada but less so in the U.S. In fact, AirMiles came and left in the U.S. One successful example here in the U.S. would be a program like UPromise, but that is in relative penetration terms a far smaller program that Canadian hub rewards programs.

Collins said what is happening now in Canada is an “ante-upping” of rewards value.

“There are several co-brand programs that are underwhelming from a value perspective and that is changing rapidly,” he explained. “The entrance of far more aggressive issuers from across the border is having a big influence.”

Collins said what Rogers is doing in Canada regarding starting a bank is “much more frowned upon” by regulators in the U.S.

“While it isn’t a slam dunk in Canada and will take a while to get fully approved, it is an area in which Canada is more progressive than the U.S.,” Collins said. “It would be very hard for, say, Verizon here in the U.S. to get approved for a captive bank. There are advantages to such a structure, but more risk. It comes down to the type of banking and lending behavior that Rogers creates in its marketing and product line. Positive selection for both credit score and usage is important in the lending area and I am sure Rogers is focused on creating a product line that optimizes that.”

Collins said successful co-brand programs require four key factors, no matter where they are launched:

A positively credit selected customer, which is driven primarily by a great value proposition that is truly breakthrough and unique

A co-brand partner that weaves the program into the entire customer experience and underlying rewards program, and treats the product like one of its core offerings -- not just a ride-along. That usually means performance measurement, executive leadership and accountability, and incentives to the front line.

An issuer and payment network intimately focused on the partner’s broader corporate objectives, not just the silo of the credit card portfolio

Financial alignment between all parties – meaning the end customer, the partner, and the issuer – to equitably share the program benefits. This means a value proposition and deal structure that is in alignment with this goal. Much easier said than done.

Collins believes that what Rogers is pursuing to use the co-branded credit card program to enhance its customer loyalty program is a “great use” and most successful programs follow the same path.

“Some of the similar efforts in the U.S. have been less successful in this sector than, say, travel-based loyalty programs, so it will be interesting to see how Rogers makes this an “aha” moment for its customers,” Collins said. “But generally, if there is a successful and widely participated loyalty program, that suggests good prospects for a cobrand card in general. However, the “must haves” above have to be there.”

Chairman and CEO Gary Loveman shared a few favorable results from the launch of the refreshed Total Rewards cobrand program on the Caesars' quarterly earnings call.

We're so pleased to see such success from the program so far!

“……Our recent investments to upgrade and refresh our marketing and analytics capabilities, I'm very excited about, are yielding results across the enterprise and we're really just at the beginning. The early results of the new caesars.com are quite encouraging. The site, which has been rolled out for most of our properties, has helped generate double-digit revenue increases in key metrics, including direct bookings and cross-promotion. We launched the new Total Rewards credit card partnership with Alliance Data. This partnership provides Total Rewards members with another opportunity to earn reward credits, engendering further loyalty and functionality for the program and our guests. This card program has generated far more interest than past credit card offerings, resulting in the issuance of 15,000 cards in just the first 2 weeks of availability. We're also seeing results from our investments to create a next generation analytics infrastructure. The Big Data capabilities that we've added are helping us to become more efficient, strategic and insightful in our marketing efforts, resulting in significantly enhanced customer segmentation and a higher a degree of intimacy and relevance in our offers to our guests.”

Partner Advisors served as advisor to Gander throughout the process of renewing their cobrand credit card program with Alliance Data.

Alliance Data to Continue Providing Co-Brand Credit Card Program for Leading Multichannel Retailer of Outdoor Lifestyle Products and Services

DALLAS, Feb. 28, 2013 /PRNewswire/ -- Alliance Data Systems Corporation (NYSE: ADS), a leading provider of loyalty and marketing solutions derived from transaction-rich data, today announced its Retail Services business has signed a long-term agreement to continue providing the co-brand credit card program for multichannel retailer Gander Mountain, operator of the largest network of stores specializing in fishing, hunting, camping, marine, and outdoor lifestyle and active performance products for the serious outdoor enthusiast. Established in 1960, Gander Mountain Company, headquartered in St. Paul, Minn., offers national, regional and local brands and private label merchandise through its 119 stores in 24 states, as well as through a robust e-commerce site and its Overton's catalog brand.

(Logo: http://photos.prnewswire.com/prnh/20051024/ADSLOGO )

"The strategic program offering Alliance Data brings to the table--from their card program and loyalty capabilities, to advanced analytics and marketing expertise--continues to make them the right partner to help Gander Mountain meet our sales and growth goals," said Robert Specht, vice president of finance and controller for Gander Mountain. "The Gander Mountain customer enjoys a special relationship with our brand, both in-store and online, and our credit card program helps reinforce the strength of that relationship, driving long-term customer loyalty and sales. We look forward to extending our partnership with Alliance Data to ensure the Gander Mountain co-brand credit card program continues to deliver additional value to our best customers--our cardholders."

Alliance Data will continue to deliver a marketing-driven co-branded credit card program that recognizes and rewards Gander Mountain cardholders with a tiered loyalty program offering free-merchandise rewards based on all dollars spent with Gander Mountain and Overton's, gas and grocery purchases, and on all other transactions. The program also offers flexible financing options and other cardholder-exclusive perks designed to drive brand loyalty and repeat purchases. In addition, the Gander Mountain credit card design will soon be customizable, allowing individual cardholders to display their own favorite photographs on the card plastic.

"The Gander Mountain name truly stands for quality and superior customer service. We're thrilled to continue this valued partnership, driving long-term loyalty and increasing sales through the co-brand card program, " said Melisa Miller, president of Alliance Data Retail Services. "Through this extended relationship, we will deliver even deeper value to Gander Mountain customers, resulting in overall brand and card-program growth. Together with Gander Mountain, we will continue to drive brand affinity through tailored payment promotions and customized marketing campaigns that reinforce Gander Mountain's well-respected brand."

Partner Advisors served as program advisor to Gander Mountain during contract negotiations.

About Gander Mountain Company

Gander Mountain Company headquartered in St. Paul, Minn., is the nation's largest retail network of outdoor specialty stores for firearms, hunting, fishing, camping, marine and outdoor lifestyle products and services. Since 1960, Gander Mountain has offered the best selection of outdoor equipment, technical apparel, active casual wear, and footwear featuring national, regional and specialty brands at competitive prices. Focused on a "We Live Outdoors(R)" culture, Gander Mountain dedicates itself to creating outdoor memories. There are currently 119 conveniently located Gander Mountain outdoor lifestyle stores in 24 states. For the nearest store location call 800-282-5993 or visit www.GanderMountain.com Gander Mountain is also the parent company of Overton's (www.overtons.com), a leading Internet based retailer of products for boating and other water sports enthusiasts.

About Alliance Data Retail Services

Alliance Data Retail Services is one of the nation's leading providers of branded credit card programs, with over 100 marketing-driven private label, co-brand and commercial programs in partnership with many of North America's best-known brands. The business delivers upon its Know More. Sell More.(R) commitment by leveraging customer insight to drive sales for its client partners. Leveraging deep-rooted retail industry expertise, transaction-based customer data, and advanced analytics, Alliance Data Retail Services creates turnkey, multichannel credit programs designed to help its clients develop stronger, more profitable customer relationships. Alliance Data Retail Services is part of the Alliance Data family of companies. To learn more about Alliance Data Retail Services visit www.alliancedata.com.

About Alliance Data

Alliance Data(R) (NYSE: ADS) and its combined businesses is North America's largest and most comprehensive provider of transaction-based, data-driven marketing and loyalty solutions serving large, consumer-based industries. The Company creates and deploys customized solutions, enhancing the critical customer marketing experience; the result is measurably changing consumer behavior while driving business growth and profitability for some of today's most recognizable brands. Alliance Data helps its clients create and increase customer loyalty through solutions that engage millions of customers each day across multiple touch points using traditional, digital, mobile and other emerging technologies. Headquartered in Dallas, Alliance Data and its three businesses employ approximately 11,000 associates at more than 70 locations worldwide.

Alliance Data consists of three businesses: Alliance Data Retail Services, a leading provider of marketing-driven credit solutions; Epsilon(R), a leading provider of multichannel, data-driven technologies and marketing services; and LoyaltyOne(R), which owns and operates the AIR MILES(R) Reward Program, Canada's premier coalition loyalty program. For more information about the company, visit our web site, www.AllianceData.com, or you can follow us on Twitter at www.Twitter.com/AllianceData.

Alliance Data's Safe Harbor Statement/Forward Looking Statements

This release may contain forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Such statements may use words such as "anticipate," "believe," "estimate," "expect," "intend," "predict," "project" and similar expressions as they relate to us or our management. When we make forward-looking statements, we are basing them on our management's beliefs and assumptions, using information currently available to us. Although we believe that the expectations reflected in the forward-looking statements are reasonable, these forward-looking statements are subject to risks, uncertainties and assumptions, including those discussed in our filings with the Securities and Exchange Commission.

If one or more of these or other risks or uncertainties materialize, or if our underlying assumptions prove to be incorrect, actual results may vary materially from what we projected. Any forward-looking statements contained in this presentation reflect our current views with respect to future events and are subject to these and other risks, uncertainties and assumptions relating to our operations, results of operations, growth strategy and liquidity. We have no intention, and disclaim any obligation, to update or revise any forward-looking statements, whether as a result of new information, future results or otherwise, except as required by law.

"Safe Harbor" Statement under the Private Securities Litigation Reform Act of 1995: Statements in this presentation regarding Alliance Data Systems Corporation's business which are not historical facts are "forward-looking statements" that involve risks and uncertainties. For a discussion of such risks and uncertainties, which could cause actual results to differ from those contained in the forward-looking statements, see "Risk Factors" in the Company's Annual Report on Form 10-K for the most recently ended fiscal year. Risk factors may be updated in Item 1A in each of the Company's Quarterly Reports on Form 10-Q for each quarterly period subsequent to the Company's most recent Form 10-K.

SOURCE Alliance Data Systems Corporation

Partner Advisors recently teamed up with The Motley Food as advisor in defining the new value proposition of the card program, provided guidance throughout the process of selecting a new issuer and payment network, developed program contracts, and continues to advise on program launch planning.

Two leading financial service industry providers join forces to create a dynamic, new affinity relationship. The partnership brings custom-branded PenFed credit cards and auto loans to members of one of the top, online investment advisory companies in the world today, The Motley Fool.

Alexandria, Va (PRWEB) April 24, 2013 -- PenFed (Pentagon Federal Credit Union) announced today that beginning April 24, 2013; the nationwide credit union will launch an exclusive new affinity relationship with The Motley Fool (TMF), a leading multi-media financial services company.

“The Motley Fool is extremely excited to announce our partnership with PenFed,” said Rebekah Hughes, Chief Marketing Officer. “Like The Motley Fool, PenFed is built on the core values of honesty, transparency and a passionate commitment to providing superior member service. That’s why we’ve partnered to create three unique credit cards dedicated to returning maximum value and benefits to our members through low loan rates and rich credit card rewards. Together, PenFed and The Motley Fool provide powerful financial solutions for our members.”

“We are delighted to welcome The Motley Fool to the credit union as our newest affinity partner,” said Nicole Butler, Senior Vice President of Marketing and Client Development, PenFed. “Our membership is inclusive to military members, but stretches beyond those realms to the everyday citizen. PenFed aligns with The Motley Fool in educating and enriching the lives of individuals. We look to provide unique benefits by offering a suite of award-winning credit cards, and maintaining unbelievably low rates on auto loans. This newly forged partnership will not only allow us to proudly support The Motley Fool's efforts to educate and enrich the minds of individual investors around the world, but it will open the door to new and exciting financial opportunities for their members."

The Motley Fool champions shareholder values and advocates for the individual investor. Its flagship investment advisory service, Motley Fool Stock Advisor, is the brainchild of brothers David and Tom Gardner, the investing duo recognized for their refusal to conform to traditional Wall Street practices. Their winning investment recommendations offered to Stock Advisor members have outperformed the stock market by 65.98% over the past 11 years*.

Credit Card Lending

Motley Fool members will be able to choose from three separate credit cards:

• The Motley Fool PenFed Premium Travel Rewards American Express® Card

• The Motley Fool PenFed Platinum Cash Rewards Visa® Card

• The Motley Fool PenFed Promise Visa® Card

All three credit card programs will allow Motley Fool members to enjoy highly competitive features such as low purchase annual percentage rates (APRs) and no annual fees.

The Motley Fool PenFed Premium Travel Rewards American Express® Card is one of the richest travel rewards cards in the country. This card features 5 points on airfare purchases, and valuable benefits such as complimentary 24-hour concierge services, comprehensive travel insurance coverage, and rich rewards points that are redeemable for travel, gift cards, and merchandise.

The Motley Fool PenFed Platinum Cash Rewards Visa® Card is considered to be among the best cash rewards cards in the marketplace. This card is known for its rich value proposition and ease of use since cash rewards are automatically credited back to the cardholder’s account at the end of each billing cycle period as a statement credit with no cap on earnings.

The Motley Fool PenFed Promise Visa® Card will appeal to those individuals who are interested in a card that is simple, carries no fees, and has a low introductory purchase APR—one of the lowest APRs in the credit card industry today.

A Fool’s Paradise

For those Motley Fool members interested in joining the credit union, PenFed will open courtesy membership accounts, which will allow individuals to apply for any of the financial products this partnership offers.

Motley Fool members can establish their PenFed membership, and learn more about the affinity lending programs, by calling 866.386.7191 or visiting PenFed.org/TMF.

About PenFed (Pentagon Federal Credit Union)

Established in 1935, PenFed is one of the largest credit unions in the United States with over a million members around the world and nearly $16 billion in assets. PenFed provides an extensive selection of financial products to its members worldwide. Its core membership includes the Department of Defense, Army, Marine Corps, Navy, Air Force, and Coast Guard; Department of Homeland Security personnel, employees or volunteers of the American Red Cross, numerous military associations, and many others. PenFed is federally insured by the National Credit Union Administration and is an equal housing lender. For more information about PenFed, visit PenFed.org.

About The Motley Fool

Headquartered in Alexandria, Va., The Motley Fool is a multimedia financial services company dedicated to helping the world invest better. Reaching millions of people each month through its website, books, newspaper column, television appearances, and subscription newsletter services, The Motley Fool champions shareholder values and advocates tirelessly for the individual investor. For more information about The Motley Fool, visit www.fool.com.

*Returns as of April 16, 2013.

Partner Advisors served as advisor to Caesars Entertainment in defining the new value proposition, selecting a new issuer and payment network, developing program contracts, and continue to advise on launch planning and program growth initiatives.

LAS VEGAS and DALLAS, March 28, 2013 /PRNewswire/ -- Caesars Entertainment Corporation (CZR), a leader in hospitality and entertainment, today announced it is partnering with Alliance Data Systems Corporation's (ADS) Retail Services Business, a leading provider of loyalty and marketing solutions, to launch a new Total Rewards credit card, providing another way for the loyalty program's members to earn credit in the award-winning loyalty program.

In partnership with Caesars, Alliance Data will launch the Total Rewards Visa co-brand credit card, enabling cardholders to accelerate their earnings through Total Rewards program for purchases made at Caesars' resorts as well as on all other purchases made with the card outside of Caesars locations. In addition, premier Total Rewards Visa Signature® cardholders will have access to all of Visa Signature's benefits, including travel, entertainment, sports and travel protection benefits. Caesars' Total Rewards loyalty program, winner of Colloquy's 2012 Master of Enterprise Loyalty award, sets the industry standard in recognizing and rewarding members based on their engagement across Caesars resorts, including dining, entertainment, hotel stays, shopping and more.

"At Caesars, we focus on building relationships and loyalty with our guests through a distinctive combination of great service, memorable experiences and unmatched rewards. These also are the attributes we sought in a partner to help us grow our credit card program, and to help provide our guests new opportunities to earn benefits through Total Rewards," said Joshua Kanter, SVP of Total Rewards at Caesars Entertainment. "Alliance Data brings a comprehensive suite of tools that will enable our guests to easily and conveniently join our new credit card program. Alliance Data's purchase data and customer profiling tools will allow us to gain even deeper insight into our guests' preferences and shopping behaviors."

"We are excited by this strategic partnership with Caesars Entertainment and are dedicated to working with Caesars to enhance the industry-leading Total Rewards program. Together, we will bring on new cardholders and ensure that these Caesars customers are rewarded in ways that are increasingly meaningful and valuable to them," added Melisa Miller, president of Alliance Data Retail Services. "We look forward to collaborating closely with this dynamic company to enhance its brand affinity and drive sustained loyalty among its valued guests. This new partnership also extends Alliance Data's commitment to the hospitality category – a key growth vertical for Alliance Data Retail Services."

Alliance Data will enable Caesars to develop a deeper understanding of its cardholders through analysis of purchase behaviors, and will also help Caesars to further engage cardholders through expanded customer-relevant channels – all to increase cardholder loyalty to the Total Rewards program and the broader portfolio of Caesars brands. Caesars will also have access to Alliance Data's advanced set of digital and mobile capabilities connected to the card program, which will give Caesars customers the convenience of using their smartphone to apply for the Total Rewards credit card. All credit card accounts will be targeted to customers that meet Alliance Data's traditional credit quality standards.

Full Article

Source: Yahoo! Finance

Loyalty360 features several columnists each month to provide insight into the world of loyalty marketing. This month, Partner Advisors' Jonathan Gelfand was featured with his article "Following the Money". Check out Jonathan's work below or visit the site to see all of March's featured contributors.

Partner Advisors has recently become a gold level sponsor of Loyalty 360!

Read More ›